In 2023, the modern retail business gradually improved in line with the economy. The main drivers were:

- Government stimulus measures

- The gradual return of foreign tourists

- Middle- and upper-income consumers still have significant spending potential

- Online sales also helped to boost sales to some extent

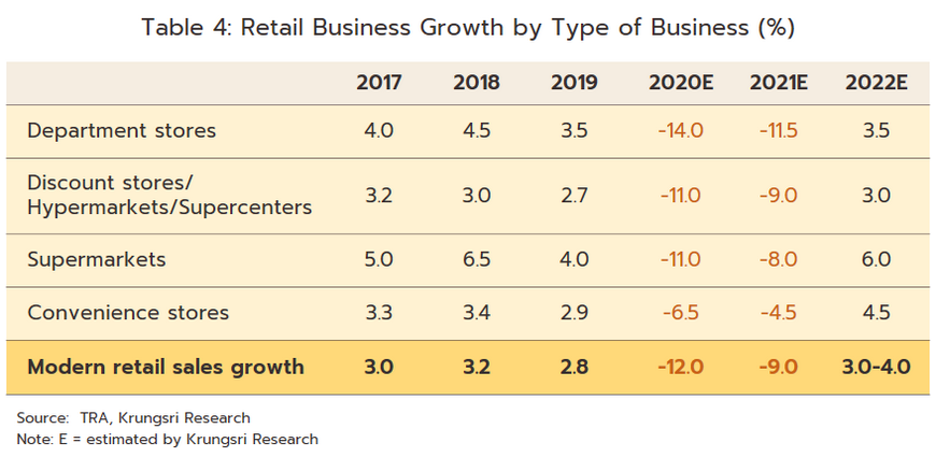

However, the purchasing power of most people was pressured by rising living costs, causing sales to grow only slightly at 3.0-4.0%.

For 2024-2026, the business is expected to grow at an average rate of 4.0-5.0% per year, driven by:

- Rising purchasing power, following the expected average growth of the Thai economy of 3.0-4.0% per year

- The number of foreign tourists is expected to return to pre-COVID-19 levels by 2026

- Megaproject investments will help to create jobs and increase money circulation in the system

- Economic growth in neighbouring countries will create opportunities for businesses to generate revenue

The direction of the modern retail business is expected to expand physical stores in parallel with the development of online marketing channels, new business models, and the widespread use of technology. This will help create differentiation and increase the business’s competitiveness amid increasing competition from operators expanding their customer base to be wider and more comprehensive to support long-term revenue growth.

Modern retail businesses are expected to recover in line with consumer spending, especially with the gradual return of foreign tourists, which is expected to increase at an accelerated rate. The progress of infrastructure investment will also lead to the expansion of modern retail businesses. However, the competition in the business is expected to intensify amid the high level of household debt. The growth of each type of business is as follows:

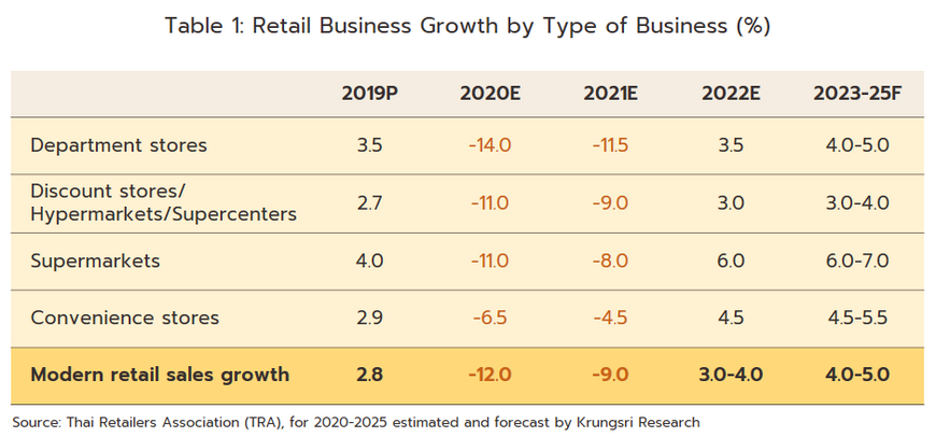

Department stores: Sales are expected to accelerate significantly by an average of 4.0-5.0% per year from 3.5% in 2022. This is due to the easing of COVID-19 concerns and the adjustment of strategies by operators. They focus on developing omnichannel platforms and using 5G and AR technology to create a better consumer experience. Additionally, they are expanding their investments into countries with promising market potential, which will help to support continued revenue growth.

Discount stores/hypermarkets/supercenters: Sales are expected to grow by an average of 3.0-4.0% per year from 3.0% in 2022. This is due to the expansion of branches by operators in various formats suitable for the area and spread across the country. This allows them to reach a wider range of customers. They also continuously develop digital platform channels and sell products at lower prices than other stores. However, the business will face intense competition as most of the products sold are not differentiated or are similar to those sold in other retail formats.

Supermarkets: Sales are expected to grow at 6.0-7.0% per year from 6.0% in 2022. This is the highest growth rate compared to other types of retail businesses. This is due to the marketing strategies that align with the behaviour of consumers, who are mostly middle-upper to upper-income customers with high purchasing power. Supermarkets have strengths in product quality and have various strategies, such as:

- Adjust the store format to a premium lifestyle supermarket focusing on expensive imported products.

- Expanding branches in provinces with high purchasing power.

- Continuously developing online sales formats to facilitate consumers.

Supermarkets also have the advantage of scaling and expanding branches in large communities, resulting in continued performance.

Convenience stores/minimarkets: Sales are expected to grow by an average of 4.5-5.5% per year from 4.5% in 2022. This is due to the large number of branches spread across all areas. They have also added ready-to-eat food products and expanded online sales services. However, the competition in the business is expected to intensify due to the opening of branches by competitors in the same area and indirect competitors, especially hypermarkets that are entering the market in the form of small stores. Additionally, the networks of major operators through traditional shops are expanding, resulting in lower sales per branch for convenience stores. Convenience stores that own franchises can continue to profit, while general convenience stores will be more at risk in their operations.

Overall, the modern retail business is expected to grow at an average of 4.0-5.0% per year over the next three years. However, businesses must face increasing competition and adapt to changing consumer behaviour.

Basic information

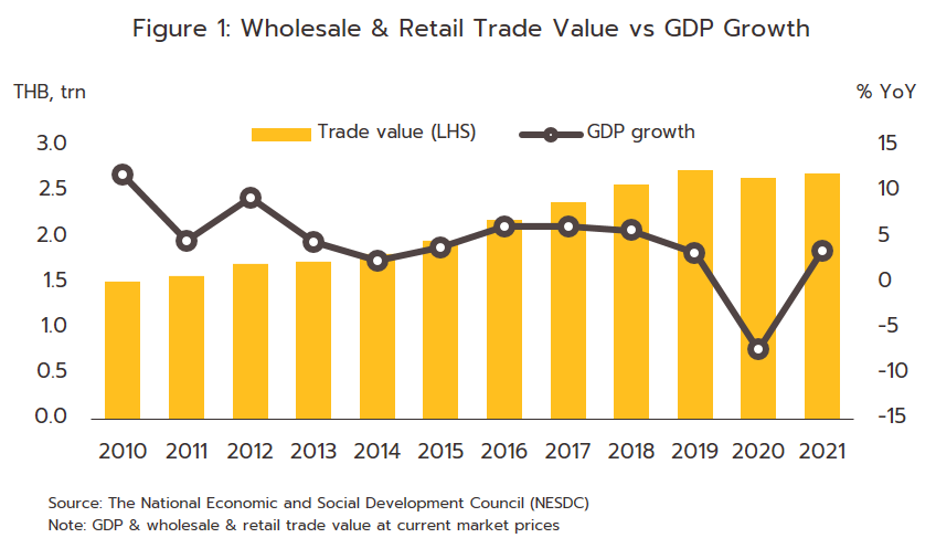

The modern retail business (Modern Trade) is part of the wholesale and retail activity, with a value of 2.7 trillion baht in 2021, up 1.9% from 2020. It accounts for 16.7% of GDP, second only to the manufacturing sector, which accounts for 27.0%. Operators are often major investors with large networks of branches and are major buyers, so they have bargaining power over manufacturers or distributors. They systematically manage their stores, including modern transportation and distribution systems, as well as adding online channels and using various technologies to gain a competitive advantage.

Modern retail stores in Thailand are growing rapidly, especially in Bangkok and major cities with high urbanisation. The main drivers are:

- Government policy that opens the door for foreign investors with modern management technology to invest in the retail business.

- The characteristics of the stores meet the needs of consumers who want convenience. For example, consumers can buy various products in one place, from food to personal care products and household items. In addition, the prices of products are often lower than in traditional retail stores.

- Continuously expand branches to expand the customer base.

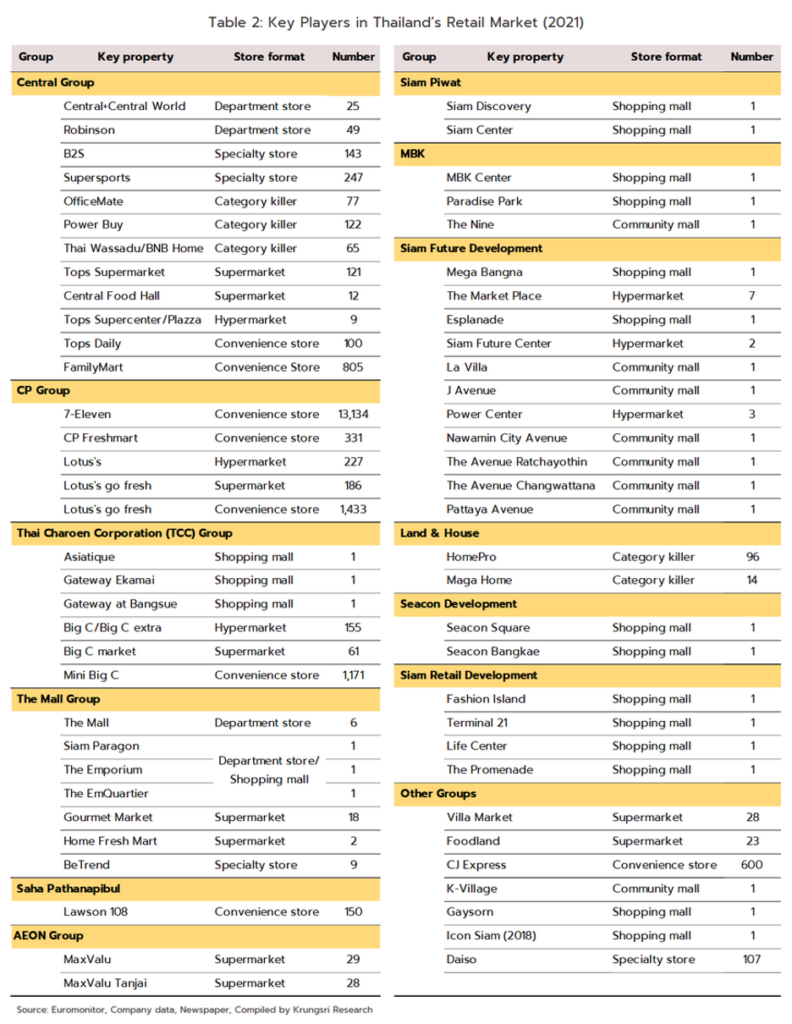

Most modern retail operators are large Thai companies with stable businesses, potential, and income-generating capabilities. This is due to their advantages in terms of size, capital, branch networks, and continuous business expansion in various forms, such as Central Group, Charoen Pokphand (CP) Group, Thai Charoen Corporation (TCC) Group, The Mall Group, and Saha Pathanapibul Group (Table 2).

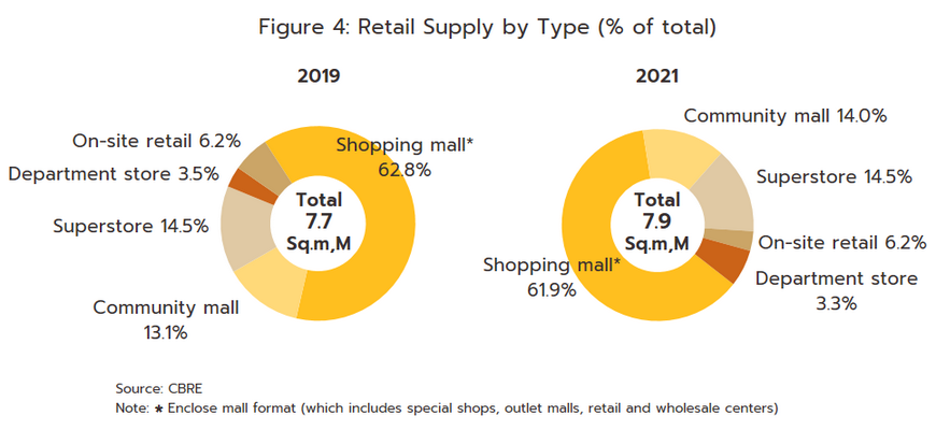

The COVID-19 pandemic has gradually expanded modern retail outlets in Thailand between 2020 and 2021. In Bangkok and the Metropolitan Region (BMR), the accumulated retail space increased by 1.3% in 2021 to 7.93 million square meters (Figure 4). The area of shopping malls and department stores (61.9% and 3.3% of the retail space in BMR) remained relatively unchanged from 2020. Community malls (14.0%) increased by 8.3% (compared to 1.1% in 2020), supermarkets (14.5%) increased by 1.6%, and supporting retail space (6.2%) increased by 0.3%.

Major modern retail operators such as 7-Eleven, Lotus, and Big C continued to expand their branches in the provinces. Also, they expanded their networks by partnering with traditional convenience stores scattered throughout the country.

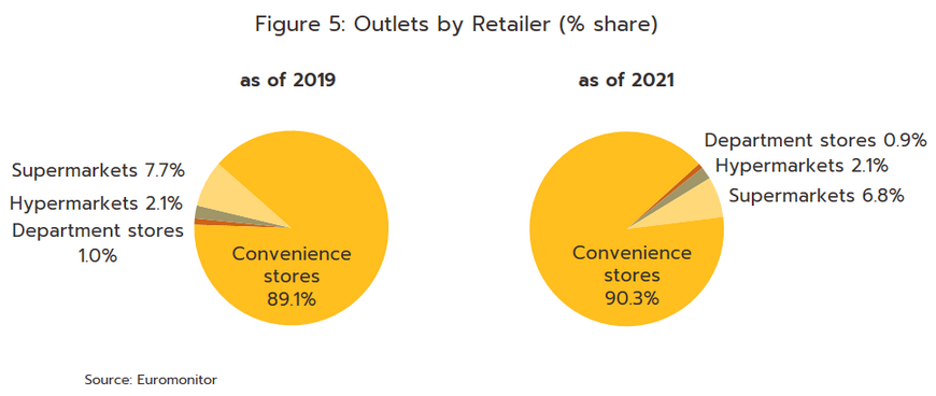

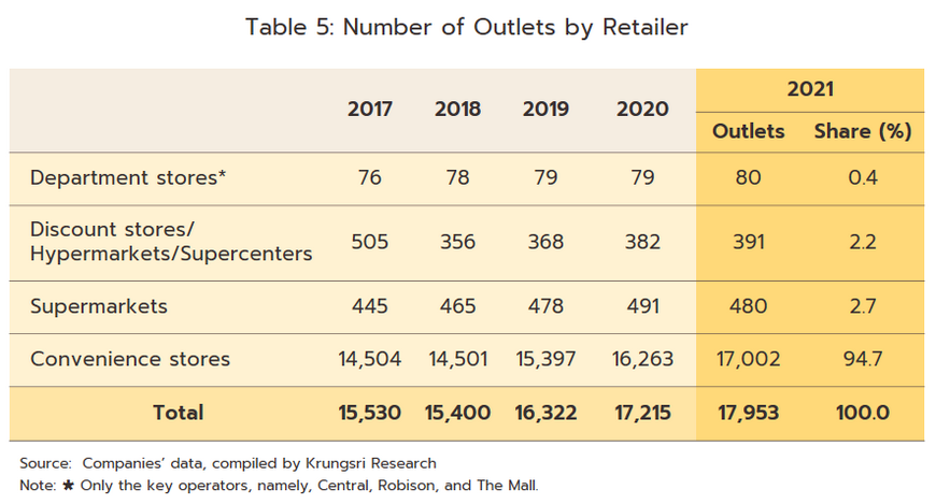

Considering the number of branches, we find that at the end of 2021, convenience stores had the highest share of branches at 90.3% of all modern retail branches, up from 89.1% in 2020. Supermarkets, hypermarkets, and department stores followed in order (Figure 5).

The modern retail business has been in a slump due to the spread of COVID-19 in multiple waves that began in 2020. However, it began to recover in late 2021 as the government gradually relaxed the strictness of disease control measures (such as reducing curfew hours and extending store operating hours) and gradually relaxed the criteria for opening to foreign tourists during the end-of-year holidays. This resulted in an improvement in overall economic activity.

In 2022, the sales of modern retail businesses continued to improve and are expected to grow by 3.0-4.0%, compared to a contraction of 9.0% in 2021. This is due to the following factors:

- Economic and social activities have returned to almost normal after the government announced that COVID-19 is a surveillance disease on October 1.

- The gradual opening of foreign tourists since the beginning of the year and the cancellation of the Test & Go system, as well as the full opening of the country for those who have been fully vaccinated since May 1, 2022, and the cancellation of the Thailand pass registration (July 1, 2022). As a result, there have been 5.7 million tourists entering Thailand (January-October). The number of foreign tourists for the whole year is expected to be 10.4 million, an increase from 430,000 in the previous year. This has helped to support retail businesses in tourist areas or with a target group of foreign tourists.

- Agricultural income has continued to improve (up 14.4% YoY in the first 9 months of the year). This has led to increased spending.

- Government spending stimulus measures, such as the 4th and 5th phases of the “Half and Half” program (March-April and September-October), the “Shop, Spend, and Get Back” program (from January 1-February 15), and the 4th phase of the “We Travel Together” program (July-October).

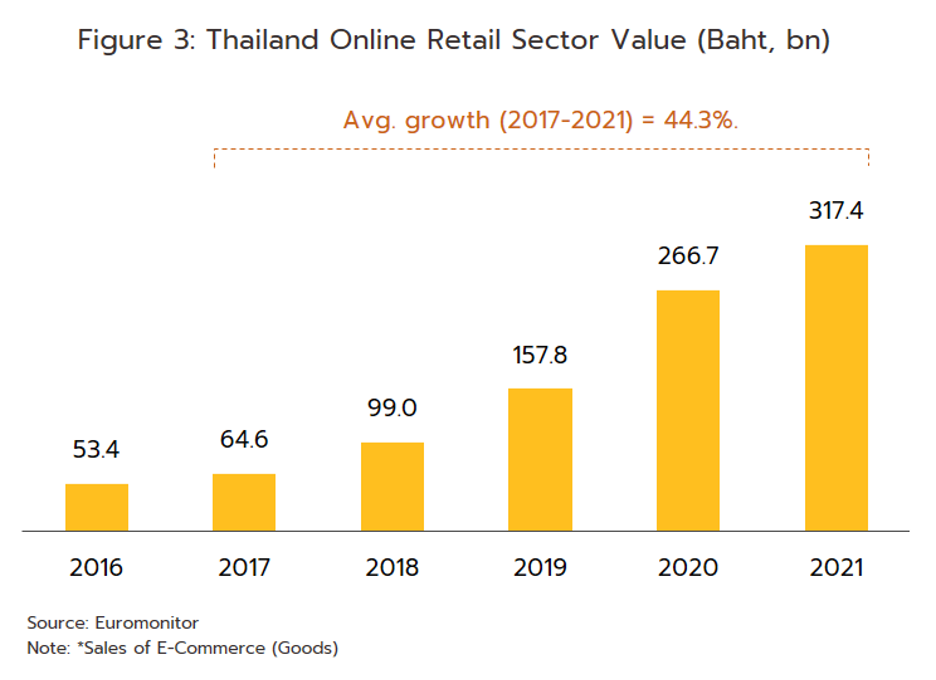

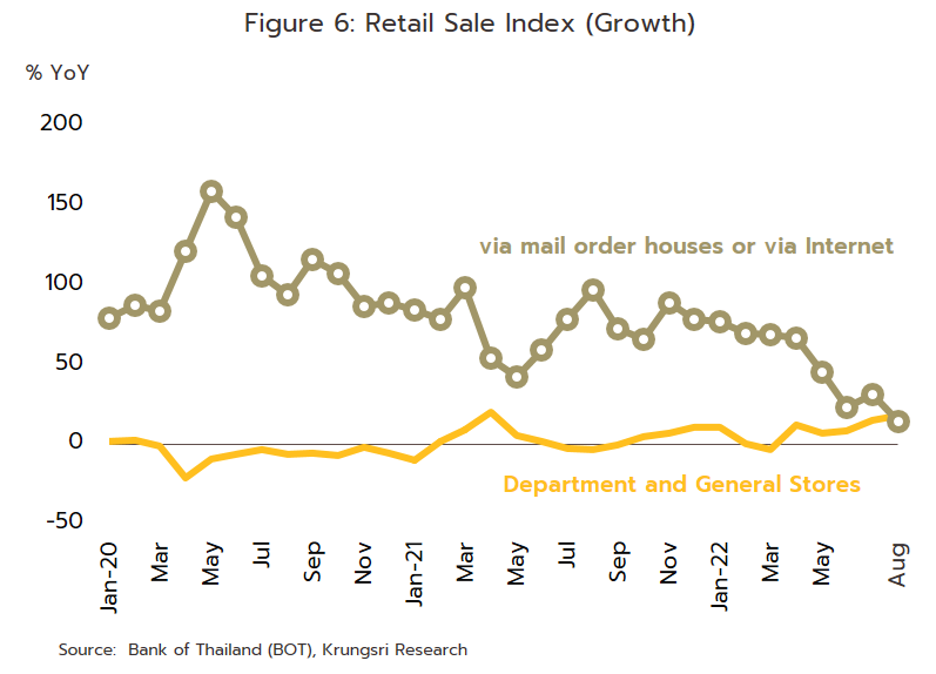

- The continued growth of the e-commerce business, as reflected by the index of goods ordered by mail, television, radio, telephone, and internet, increased by 45.9% YoY in the first 8 months (Figure 6). Meanwhile, the online order volume of operators such as Lotus has grown by more than 400% from the previous year. This is in line with the Global Digital Stat 2021 (by We Are Social and Hootsuit), which reports that the rate of online shopping in Thailand is the third highest in the world. Consumers choose to buy the most health products, fashion products, electronic products, baby and child products, and pet products. Priceza expects the E-commerce market in 2022 to grow by 30% from 2021.

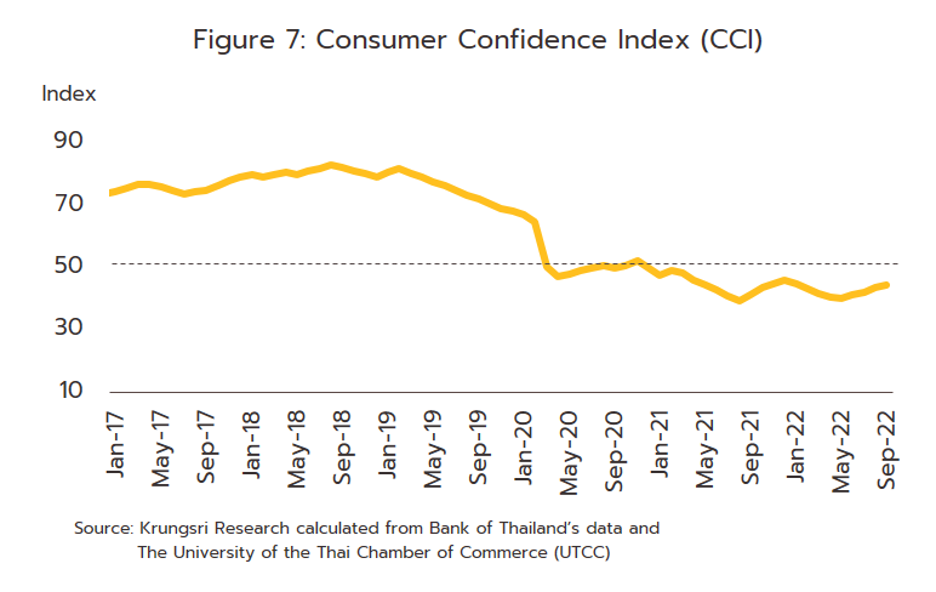

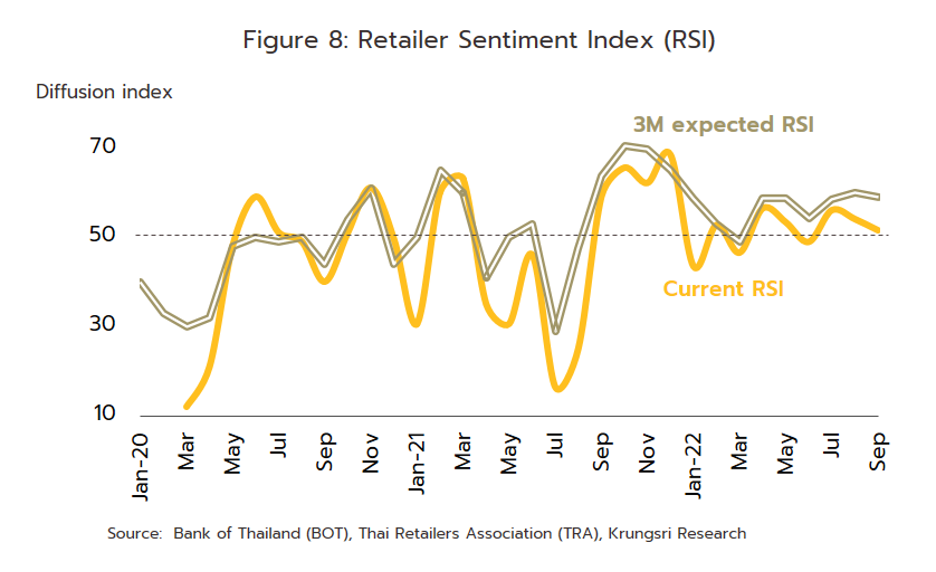

Despite signs of recovery, the retail business is still under pressure from rising living costs due to inflation, which has eroded consumer purchasing power, especially for middle- and lower-income groups that have not fully recovered. In addition, rising interest rates have increased the burden of household debt. (The Thai Chamber of Commerce survey estimates that household debt at the end of 2022 will be 89.3% of GDP, the highest in 16 years, from 88.2% in the second quarter.) For middle- and upper-income groups, spending is starting to slow down, as reflected by the consumer confidence index, which fell to its lowest level in 10 months in May (Figure 7). This is also in line with the fluctuating retail confidence survey trending downward (Figure 8). The survey found that consumers are spending more per receipt (Spending per bill) due to higher prices, while the frequency of spending has only increased slightly and is focused on essential items. (Source: Bank of Thailand and Retail Association)

Modern trade retailers continue to expand their branches, especially convenience stores that open branches in community areas, shopping centres, community malls, and supermarkets that expand retail space or open new ones. (In the second quarter of 2022, the area of community malls increased by 2.0% YoY, and supermarkets increased by 3.0% YoY.) In addition, most operators have also adjusted the format of their stores and products, such as adjusting the packaging format to meet the needs of consumers in terms of hygiene and developing e-commerce distribution channels to support the behaviour of consumers who are turning to digital platforms to order goods more and more. These include:

- Using digital platform omnichannel, such as opening an online store through a website, developing a mobile application, providing online delivery services (Quick commerce), and collaborating with other online platform businesses (Online marketplace) such as Lazada, Shopee, and JD Central.

- Doing online to offline (O2O) marketing, such as providing personal shopper services (personal shopping services), call & shop, and chat & shop, selling through social media (Social commerce) such as Facebook, Line, and e-ordering, etc.

- Accepting payment for goods through digital payment channels, such as Alipay (online banking), WeChat Pay, and Dolfin, as well as through the online system of domestic banks.

The sale of goods online allows operators to increase their points of sale and reach their target audience more widely.

Discount stores/Hypermarkets/Supercenters: Operators focus on smaller floor space, especially in Bangkok and the metropolitan area.

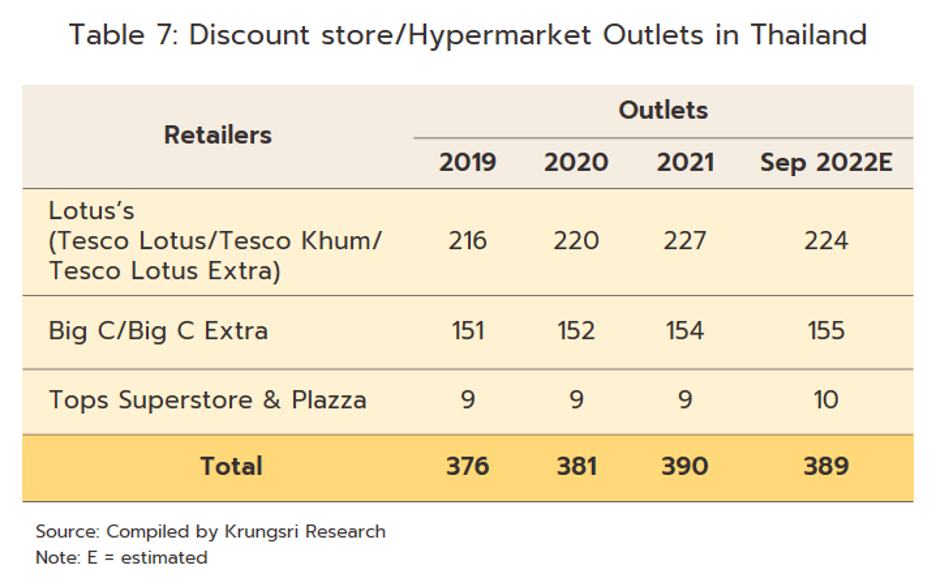

The business is quite competitive and has to compete with other retail stores, such as convenience stores, supermarkets, and speciality stores. In addition, operators from other formats are also expanding into the hypermarket business (such as Central Opening Tops Club) and the hypermarket business in the provinces. Operators also expand their investments to neighbouring countries, including Vietnam, Laos, and Cambodia, to build a long-term revenue base. However, the COVID-19 pandemic has slowed down the rate of branch expansion. 2022 the business had 2.4% more branches than in 2021 (Table 7), compared to an average of 2.7% per year between 2022 and 2023. As of the first 9 months of 2023, there were 389 branches.

The COVID-19 pandemic has led operators to develop more online marketing channels, using the omnichannel model and developing new distribution channels to stimulate sales. These include ordering products by phone or via Line, providing drive-thru services (order, pay, and wait for the product without having to get out of the car), click & collect services (order products online and pick them up at the branch), and shopping online express delivery services within 1 hour. They have also partnered with e-commerce platforms like Lazada and Shopee and social media platforms like Facebook and Line.

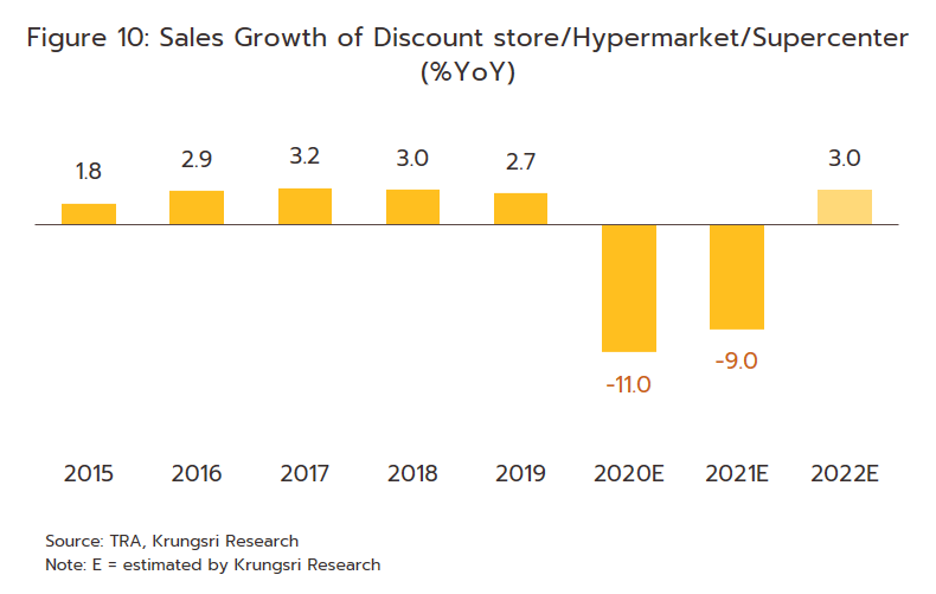

In 2023, even though the COVID-19 situation has eased, the business’s sales have been pressured by still-unsatisfactory purchasing power and rising prices. This is reflected in the fact that the index of confidence of hypermarket operators hit a 12-month low in June. However, in the remaining months of the year, the economy’s gradual recovery, government spending stimulus measures, including topping up the welfare card (over 5 billion baht), increased purchasing power from foreign tourists, and the onset of the end-of-year festival season, will support sales growth. Krungsri Research estimates that sales in 2023 will grow 3.0% from a contraction of -9.0% in 2022 (Figure 10).

Supermarkets: Continued high growth

In 2023, the business’s sales recovered well from economic activities that returned to near normal. However, the rising cost of living has accelerated, causing some consumers to spend more cautiously. Operators are accelerating their marketing strategies to align with consumer behaviour, such as:

- Developing online sales formats (such as creating a membership system to record product information) and personalising marketing through direct mailing, SMS, Line, and mobile applications.

- Adjusting the format of some branches to premium lifestyle supermarkets (such as Big C Food Place). In addition, there has been an increase in the import department of expensive products to serve customers with high purchasing power, as well as aggressive branch expansion in new retail areas such as community malls (Q2/2023, community malls in BMR increased 2.0% YoY) and stand-alone branches in provinces with high purchasing power (such as provinces with industrial estates or secondary cities with tourism potential). As a result, there were 503 branches in the first 9 months (Table 8), an increase of 4.8% from the end of 2022.

- Partnering with other operators to make it more convenient for consumers, such as GrabMart and Kerry Express.

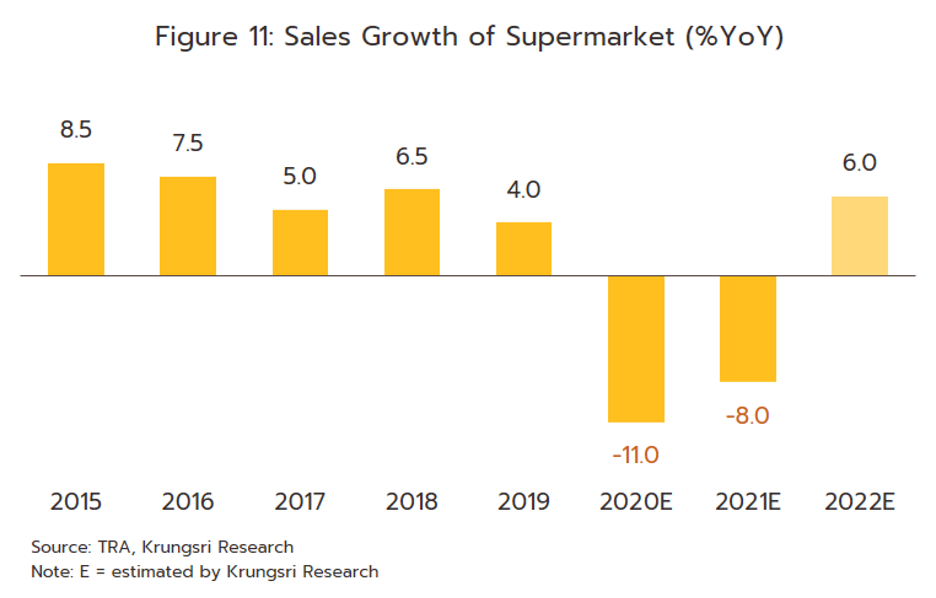

The above factors have led to the business’s sales forecast to accelerate at 6.0% from a contraction of -8.0% in 2022 (Figure 11).

Convenience stores: Have the most branches and can steal a lot of market share from traditional retail stores

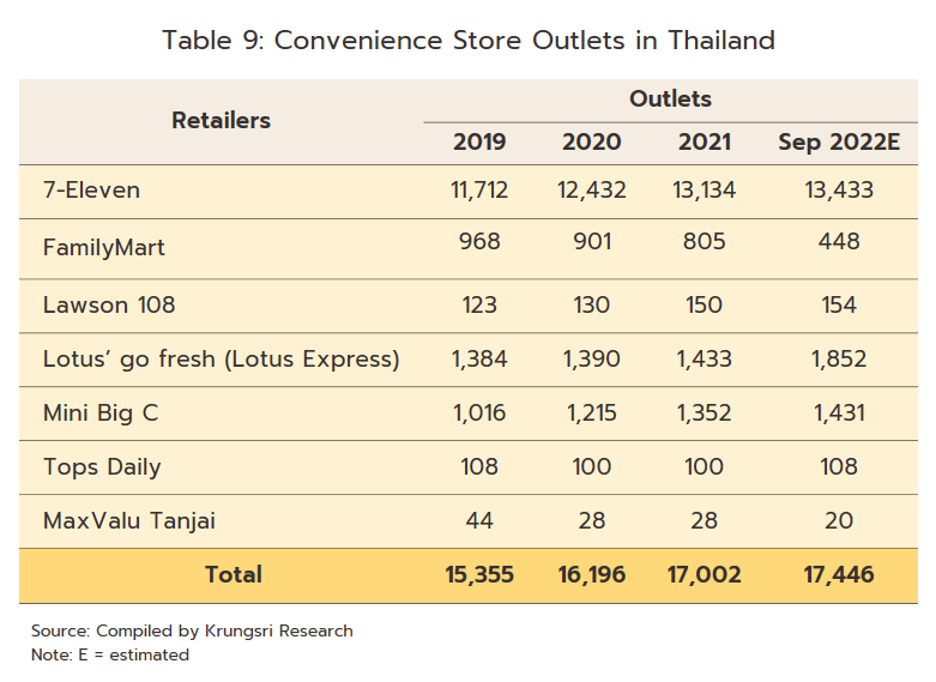

In 2023, the number of convenience stores in Thailand was 17,446, with 7-Eleven having the most branches at 13,433 (77.0%). Lotus’s Go Fresh had 1,839 branches (10.6%), and Mini Big C had 1,274 branches (8.2%). The locations of these stores include stand-alone stores with large areas, gas stations to serve travellers and surrounding communities, and stores in shopping centres.

The competition in the convenience store business is increasing both in terms of marketing and the types of products sold, such as ready-to-eat food and fresh food. Businesses are also adding utility bill payments, credit card payments, delivery, parcel delivery (in partnership with logistics providers and e-commerce providers), and vending machines.

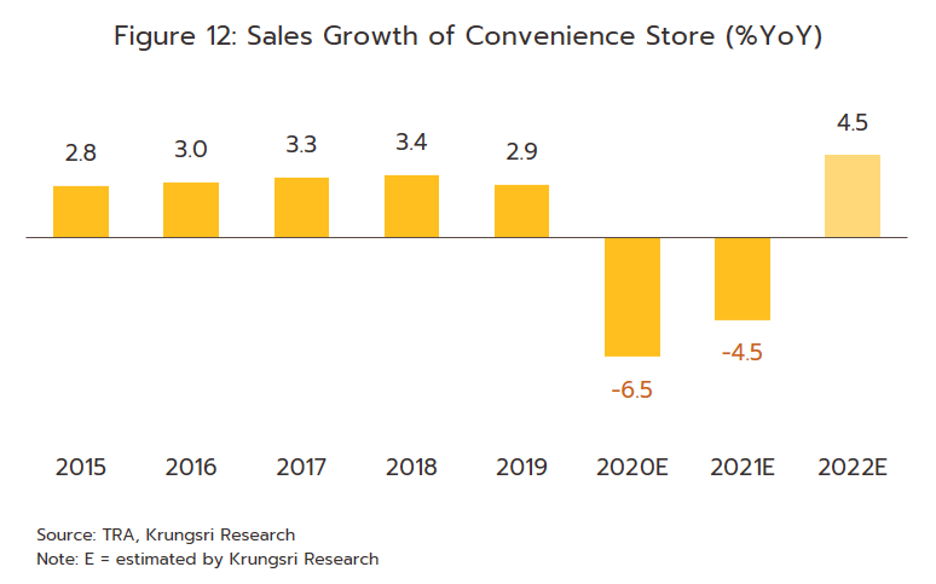

The convenience store business is expected to recover in 2023, following the improvement in economic activities and higher agricultural income, as well as government spending stimulus measures such as “We Travel Together Phase 5.” Businesses are expanding their branches to increase their customer base, including low-income consumers. They also focus more on online sales by developing platforms that connect stores, adding delivery services, and supporting mobile payment and credit card systems. These efforts have helped to stimulate sales to some extent. However, the business is under pressure from weak purchasing power, especially among middle-income groups, due to rising prices and the cost of living. As a result, the business is expected to grow by 4.5% in 2023, up from a contraction of -4.5% in 2022 (Figure 12).

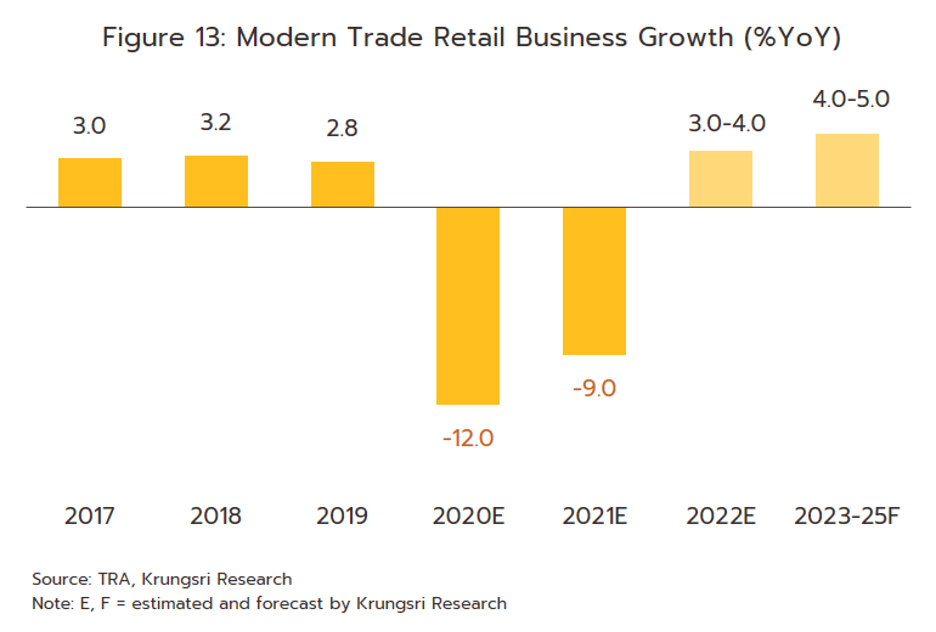

The modern retail business is expected to recover in 2023-2025, averaging 4.0-5.0% growth yearly (Figure 13). The following factors support this:

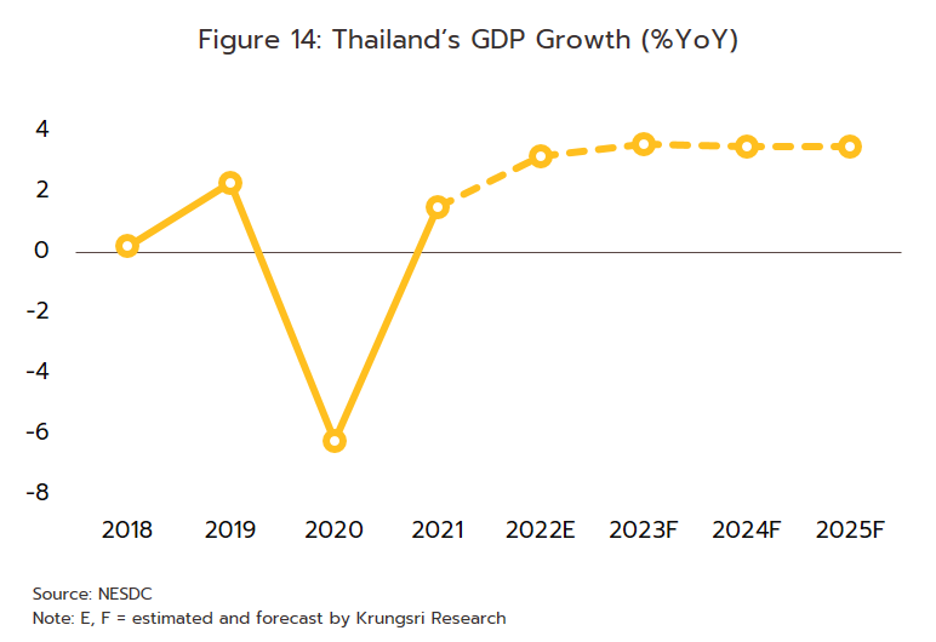

- Increased purchasing power: The Thai economy is expected to grow 3.0-4.0% yearly (Figure 14).

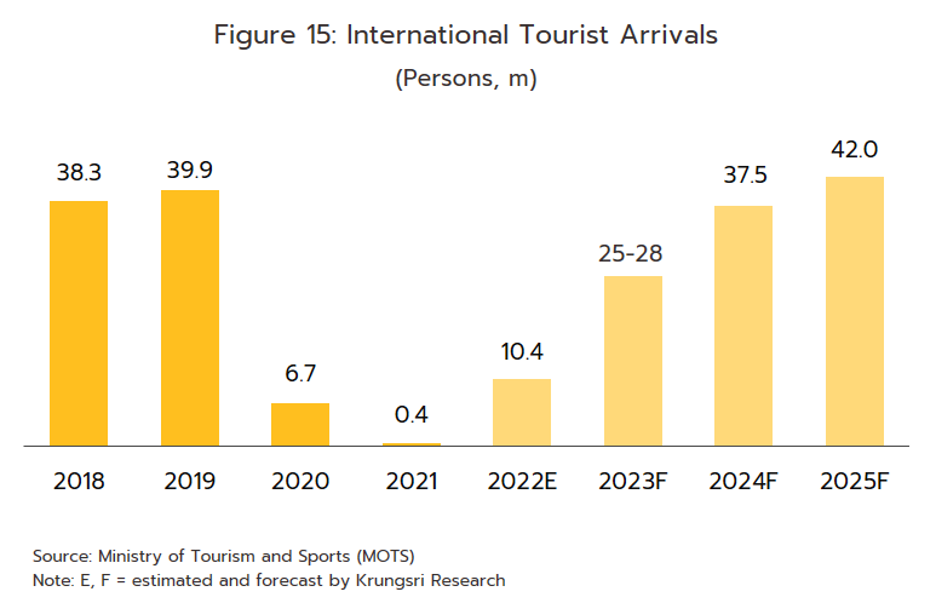

- Recovery of the tourism industry: Both domestic and international tourists are expected to increase continuously and reach pre-COVID-19 levels (domestic tourists will reach 185 million trips (similar to 2019) by 2024, while international tourists will increase to 42 million by 2025) (Figure 15). This will support the revenue of retailers in tourist areas.

- Continuing investment in mega-projects by the government will generate money circulation in the system, create jobs, and increase income. This will also support the expansion of modern retail stores.

- Continued growth of the online retail sector: This is expected to grow at an average rate of 13.6% per year (source: e-Conomy SEA 2021).

- Government spending stimulus measures: These include the increase in the minimum wage (effective October 1, 2022), which will support domestic consumption. The issuance of visas to allow foreigners with high spending potential to reside in Thailand on a special basis (4 groups) [9] will increase spending.

- Economic growth of neighbouring countries (CLMV): The IMF estimates this will be 3.5-6.5%. This will create business opportunities for retailers in the region’s border and key provinces.

Business outlook for modern retail by type

Department stores:

- Sales are expected to accelerate significantly at an average of 4.0-5.0% per year, from 3.5% in 2022. This is due to the easing of COVID-19 concerns and retailers’ adjustment of business strategies. Retailers focus on developing omnichannel platforms and using 5G and AR technologies to create a better consumer experience. Additionally, retailers are expanding their investments to countries with potential markets, which will help to sustain revenue growth.

Discount stores/hypermarkets/supercenters:

- Sales are expected to grow at an average of 3.0-4.0% per year from 3.0% in 2022. This is due to retailers expanding their branches in various formats that are suitable for the area and spread throughout communities across the country. This makes it easier for retailers to reach a wider range of customers. Retailers are also developing digital platforms and selling goods at lower prices than other stores. However, the business will face intense competition as most of the goods sold are not differentiated or are similar to those sold in other retail formats.

Supermarkets:

- Sales are expected to grow steadily at 6.0-7.0% per year, from 6.0% in 2022. This is the highest growth rate compared to other types of retail stores. This is due to the marketing strategies that align with the behaviour of consumers, who are mostly middle-upper to upper-class customers with high purchasing power. Supermarkets also have a strong point in terms of product quality and have various strategies, such as:

- Adjusting the store format to a lifestyle premium supermarket that focuses on expensive imported goods

- Expanding branches in provinces with high purchasing power

- Developing online sales formats continuously to facilitate consumers

Supermarkets also have a size advantage and are expanding branches in large communities. This has resulted in good performance for supermarkets.

Convenience stores/minimarkets:

- Sales are expected to grow at an average of 4.5-5.5% per year from 4.5% in 2022. This is due to the large number of branches spread throughout all areas. Convenience stores are also increasing the number of ready-to-eat food products and continuing to add online sales services. However, the competition in the business is expected to intensify due to the opening of branches by competitors in the same area and indirect competitors, especially hypermarkets that are entering the market in the form of small stores. Additionally, the networks of major operators are expanding through mom-and-pop stores. This has resulted in lower sales per branch for convenience stores. However, franchise convenience stores can still profit, while general convenience stores will have more business risks.